Working Papers

Several risk-related topics that merit deeper exploration are addressed in dedicated working papers presented in the following section.

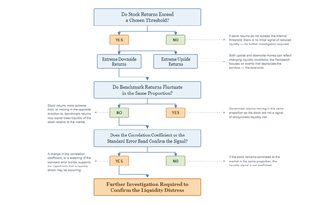

Extracting Liquidity Risk From Cross-Sectional Returns

Understanding and Measuring Liquidity Risk

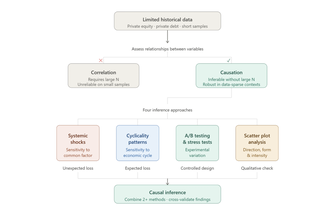

Evaluate Causation Between Variables With Limited Historical Data

Building Custom Indices in the Age of Data Abundance: From Methodology to Deployment

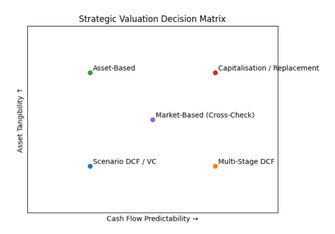

Corporate Valuation Methods

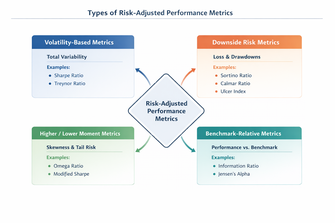

Selecting and Interpreting Risk-Adjusted Performance Metrics

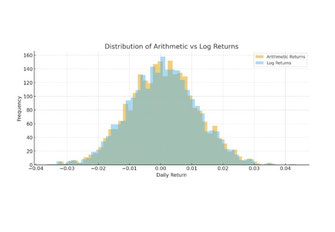

A Practical Guide To Arithmetic And Logarithmic Returns in Investment Analysis

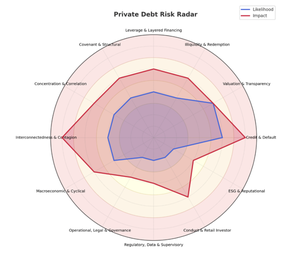

Inherent Risks in Private Credit: A Risk Taxonomy for Systemic Oversight

From Gamma to Convexity: Unified Insights into NonLinear Risk Management Across Asset Classes

Why Leveraged ETFs Lag in Performance?

This paper delves into the complexities of leveraged Exchange-Traded Funds and their performance over extended investment periods. While these financial instruments can boost returns for adept investors in the short term, they often falter in volatile or stagnant markets due to issues like volatility drag, the need for constant portfolio rebalancing, path dependency, and asymmetric returns.

Estimating Profitability of Future Investments: Highlights and Challenges

Capital budgeting is a decision-making process where an organisation assesses if a project is expected to be profitable and is worth to be funded. Many techniques are frequently used in Capital Budgeting, including IRR, MIRR, PPM, NPV, AARR, PI and EAC; this paper is dedicated to briefly get through those techniques while highlighting the pros and cons of each method.

Maximising Wealth in Unpredictable and Irrational Financial Markets

Behavioural Finance - analysing the unpredictable and irrational behaviour of investors - has become an increasingly popular discipline in the modern financial literature. This science weakened the foundations of rationale investing and shed the light on maximising wealth under irrational markets. The purpose of this paper is going through a few common-sense rules helping investors to maximise portfolio returns in irrational markets.

Risk Management in Mutual Funds

This model highlights they key Risk Management techniques to implement per Investment Strategy. This includes Debt Funds, Money Market Funds, Private Equity, Hybrid Funds, and Equity Funds.